Germany, an industrial country par excellence, is experiencing growing tourism, which in turn has become a strong driver of GDP.

Germany has recorded an increase in overnight stays of around 2.4 percent annually from 2008 onwards. Since then, overnight stays have increased from 369.6 million to more than 460 million. With an average of 5.6 overnight stays per inhabitant, Germany’s tourism intensity is rather moderate though when compared to other countries. Austria has a much higher rate of 16.5 nights per inhabitant, for example.

Taking into account the ratio of country size to its number of inhabitants, this means that Germany only manages three times as many overnight stays as Austria, even though it has almost ten times as many inhabitants. Despite this big difference, Germany is nevertheless an interesting destination. This is especially the case when it comes to its big cities, which exhibit faster market growth than the rest of the country. This is a phenomenon that applies to almost all European countries. Berlin, Hamburg and Munich especially vie for guests‘ favour in Germany. The past ten years have seen overnight stays in Hamburg rise by 6.7 percent annually, whilst Berlin and Munich have experienced an annual increase in 6.4 percent and 5 percent respectively.

What is noteworthy is that such growth isn’t just affecting the big cities – the so-called Big Seven. Growth is also evident in cities, such as Leipzig, Dresden or Nuremberg, which has in turn attracted attention from investors and hotel operators.

After 2015, 2016, and 2017, the German hotel investment market will once again exceed the EUR 4.0 billion mark in 2018 by EUR 4.020 million. A lack of supply is particularly evident in the Big Seven, which account for approximately 67 percent of the entire transactional volume. Once again, this development is pushing the average top yields of 4.10 percent to 3.75 percent.

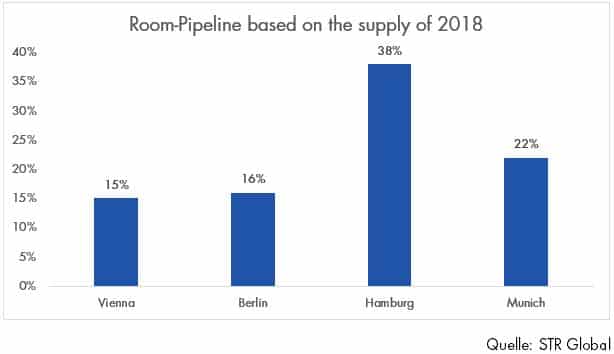

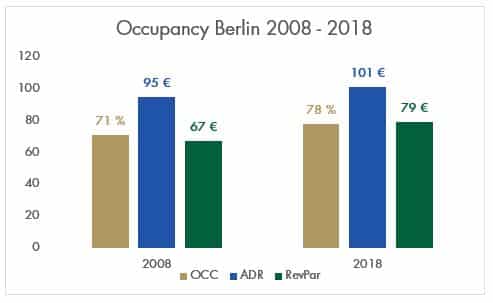

Berlin is experiencing rapid growth in its economy and mid-scale segment offerings – namely fourfold. Accounting for 56 percent of the total market in Munich and 55 percent in Hamburg, such offers account for 65 percent of the total market in Berlin, which in turn puts more pressure on the average rate. This increases the mid-scale segment (lower average rates), consequently pulling down the overall market. Approximately 10,600 rooms are currently in Berlin’s room „pipeline“, which account for roughly 16 percent of all current room listings. Existing airports are reaching their capacity limits due to the significant growth in passenger volume. In this context, the new BER airport is indispensable.

It is expected that room occupancy will increase when the airport is opened for business. Otherwise demand is expected to stagnate. If conditions remain unchanged otherwise, this could lead to a decline in occupancy rates (due to the rapidly increasing availability of rooms) from 78 percent currently to 72 percent.

Driven mainly by the national market, Hamburg has recorded a near 80 percent increase in overnight stays since 2008. 75 percent of guests are still made up of people living in Germany. Thus, the Hanseatic city still has much growth potential in terms of international guests. The hotel occupancy rate is already at 81 percent and the well-filled pipeline makes up 38 (!) percent of current room listings.

Unlike Hamburg, Munich has a balanced mix of guests, with a near equal number of national and international visitors. Occupancy is currently stagnating at 75 percent. A full pipeline will increase room availability by around 22 percent. Pressure on demand is increased so room supply grows further. The Bavarian capital has an ace up its sleeve with China. If growth remains the same, China is expected to work its way into the top 4 source markets within the next five years. Whilst Berlin and Hamburg can only dream of such things, Chinese guests could infuse tourism with a lot of momentum. Set alongside a strongly Arab-influenced summer, this would pose a new challenge for the hotel industry.